Currently, players of the 5G infrastructure market are focusing on product launches and collaborations to stay ahead of their competitors. For instance, in April 2021, Samsung Electronics Co. Ltd. launched a whitepaper on virtualized radio access network (vRAN). The vRAN is used to distribute resources freely and scale components automatically because it offers flexibility, excellent resource efficiency, and enhanced network scalability.

Other players focusing on the development and introduction of new solutions of 5G are ATT Inc., KT Corporation, SK Telecom Co. Ltd., Ciena Corporation, Airspan Networks Inc., Telefonaktiebolaget LM Ericsson, and Affirmed Networks Inc. The network architecture segment of the 5G infrastructure market is divided into 5G new radio (NR) non-standalone long-term evolution (LTE) combined and 5G standalone.

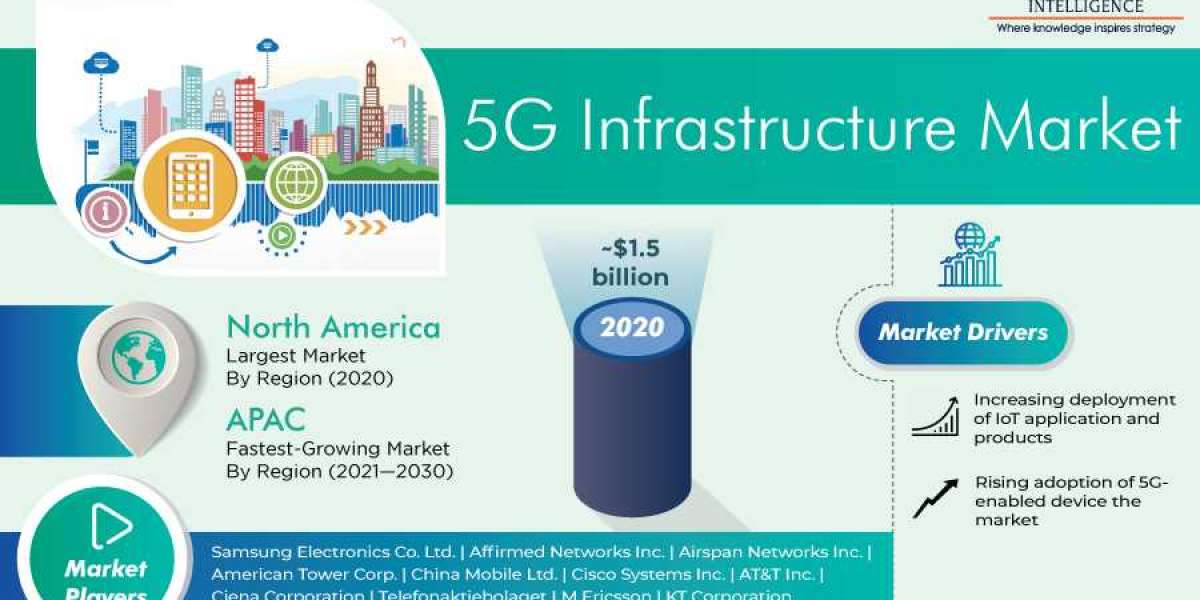

Of these, the 5G standalone (NR + core) category accounted for the larger market share in 2020, and it is expected to retain its dominance during the forecast years as well. This can be ascribed to the rising penetration of 5G-enabled devices and increasing advancements in the telecom industry. Additionally, the changing network demands of customers will also drive the growth of the market in this category.

Globally, the North American 5G infrastructure market generated the highest revenue in 2020, due to the mounting investments being made by the U.S. and Canadian governments in 5G infrastructure development. For instance, the Federal Communications Commission (FCC) created the 5G Fund for Rural America in October 2020. The FCC plans to invest $9 billion in Universal Service Fund to deploy 5G mobile wireless services in rural America.

Moreover, the surging use of advanced technologies, such as AI, IoT, autonomous driving, and wearable technologies, will also catalyze the market growth in the region. Thus, the surging demand for IoT-based products and the rising usage of network slicing in 5G infrastructure will facilitate the market growth.